By Ross Elliott, author of The Pulse

Discussions about housing affordability focus almost exclusively on the price of the real estate, movements in which are monitored by multiple organisations on a seemingly daily basis. There is comparatively little discussion about people’s incomes, which are equally as important as prices in determining what can and can’t be reasonably afforded. The income profile of what most Australian’s actually earn paints a sobering picture which could more often be taken into account in debates about housing and affordability.

It’s becoming fashionable again for business lobbies to complain about Australia’s high wage structure. It explains, they’ll argue, why we lost Holden, Ford, Toyota, and (almost) Qantas, among other things. And yes, Australia’s wages are high by competitor standards – but so are our costs. One of the most fundamental of needs, along with food and clothing, is shelter. And it’s the cost of shelter relative to incomes which has been stretched to beyond reach for a large proportion of young Australians.

Reducing minimum wages or reducing wage growth further, if at the same time allowing housing costs to further escalate, will only make this situation worse. Arguably, if we could substantially reduce the cost of supplying new housing, this would relieve upward pressure on wages and work towards improving our global competitiveness – along with repairing living standards for working and middle class families, rather than eroding them.

First, here are some of the facts on the infrequently discussed income side of the equation. (I am again indebted to the team at Urban Economics for making these available. These are top line numbers only: if you want more detailed analysis, please contact Kerrianne Bonwick).

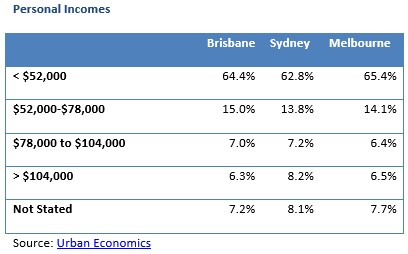

Nearly two in three of all Australians earn less than $52,000 per annum. It doesn’t much matter whether it’s Brisbane, Sydney or Melbourne; the proportion is roughly the same. It’s not much. Slightly more than another one in every eight earn from $52,000 to $78,000 per annum. Roughly eight in ten Australians earn less than $78,000 per annum.

Problem? It is if you’re trying to buy into the housing market. Take a modest house of say $400,000 (very modest depending on location). A worker on $50,000 – and these represent nearly two thirds of all workers remember – is facing a price multiple which is 8 times their gross pre-tax income.

Basically, two thirds of us are stuffed in terms of affording even a modest $400,000 property if we weren’t already in the market. A more reasonable price multiple of say 5 times income would require an income of $80,000 per annum or more. But there are less than 15% of Australians who fit this category.

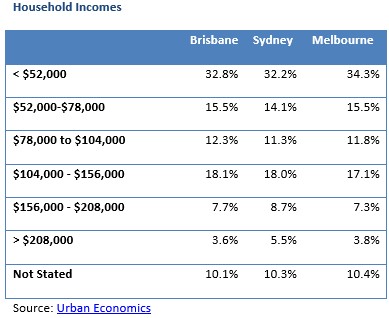

But wait, shouldn’t we count household, as opposed to personal, incomes? A good point, particularly for younger families and young couples, where dual incomes are the norm due to necessity.

But even based on combined household incomes, a third of all households earn less than $52,000 per annum. Another 14% to 15% earn between $52,000 and $78,000 and another 11% or 12% earn between $78,000 and $104,000. A reasonably healthy 30% of all households bring in a combined $104,000 per annum or more, but seven in ten bring in less than that.

Taking our modest $400,000 home again, and roughly half of all household incomes fall short of the $80,000 mark required for a price-to-income multiple of five. For one in three of every households, their combined income means a price to income multiple of eight times. They are pretty much stuffed, still.

Hang on, isn’t it more relevant to focus on the demographic that’s more likely to be trying to get into the property market, because older people and retirees, who already own or are paying off homes, may skew the figures? Absolutely: this is the key demographic, especially if you’re a developer of new detached housing product – which is what this cohort mainly wants to buy to raise a family in (as opposed to the apartment they might rent while pre-children).

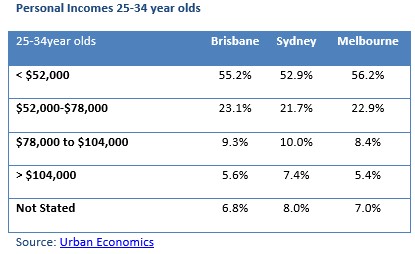

Personal income profiles of the 25-34 year old age group are pretty much in line with the Australia wide picture. More than half earn less than $52,000 and roughly eight in ten earn less than $78,000 per annum, which means eight in ten of this age group – who are at the peak of their family formation potential – would be faced with a price multiple of more than 5 times incomes on a $400,000 property, and more than half would be faced with a price multiple which is eight times their income, or more.

None of this is great news. For developers trying to provide affordable new housing in new greenfield estates in urban fringe locations, the reality of these income profiles can’t be escaped. I had the privilege of visiting one such estate in south east Queensland recently and what I saw was absolutely first class product at very good entry level prices in a very well designed environment. No ‘McMansions’ here – just quality new detached three and four bedroom homes, on small lots, priced from around $350,000 – and in some cases less.

But even at $350,000, only around 15% or so of the target 25 to 34 year old demographic could afford to get in with a price multiple of less than 5 times an individual’s income. That proportion would rise taking into account combined incomes for this age group, but it won’t rise beyond around a quarter or a third. The reality is that more than half this age group would find an entry level $350,000 home would be six times their combined incomes or more. It would be tough going.

Granted, interest rates are currently very low and some governments are offering stamp duty and other concessions to first time buyers. But these are having next to no impact on this market. Rates of first home buyer activity are at generational lows. And interest rates won’t stay this low forever. A significant rise in variable home loan rates could tip a substantial number of families in this age group from the ‘just making it’ basket into the ‘we’re stuffed’ basket.

Since the ‘do nothing’ policy approach doesn’t seem to be working, what could be done to turn the situation around? Basically, it’s a simple formula between incomes and prices. You either increase incomes or reduce prices. The first probably isn’t an option unless incomes can gradually creep up with inflation and with productivity gains over time.

But what could also happen is the cost of supplying new housing (not referring to existing stock) could be reduced. New housing is heavily taxed and over regulated (the same cannot be said of existing stock). Something like a quarter to a third of the cost of the new home in an urban fringe location is due entirely to various taxes, charges and compliance costs (which do not apply to existing stock). It is also affected by the rapid escalation in land costs due to policy induced supply constraints in areas of ample available land (the same can’t be said of existing stock in mostly built-out inner or middle ring areas). Most of these additional costs of supply owe themselves to policy changes made since the early 2000s – precisely the time when the affordability gap began to widen. It does seem a compelling place to start.

We should aspire to a more competitive Australia but this policy effort cannot just focus on labour costs because our incomes, while high by competitor standards, are now generally insufficient to cover one of the basic necessities of life: shelter. We have made this happen because policy makers have deliberately increased the cost of delivering new housing with new taxes, charges and compliance costs, all justified on esoteric planning or sustainability principles but impossible to justify on social equity or economic grounds.

These policy changes were made to suit political agendas at the time: they were not needs-based or market-based policy changes. (It also has to be said the political agendas at the time were in the hands of Labor State governments, starting with Bob Carr in NSW but which spread rapidly to other jurisdictions. Why Labor Governments introduced policies which hurt people on working wages is as mystifying to me as why Liberal Governments have continued to maintain the same policy positions, with little amendment).

The gap between the cost of supplying even relatively basic housing on the urban fringe, and the incomes of the people who in past generations could afford it, will continue to widen unless regulators and policy makers begin to grasp the wider economic consequences of policy-inflated costs for new housing supply.

Footnote: why a five times multiple? There is no strong reason. The authors of the global housing affordability report Demographia will argue that affordable housing should be around three times incomes. Moderately unaffordable they define as between 3 and 4, and between 4 and 5 is defined as ‘seriously unaffordable.’ The multiples of 7 or 8 times incomes, which we’re seeing in Australia, are off the scale. But for the purpose of argument, if even relatively high (by international standards) multiples of 5 times incomes seems like a utopian dream, it illustrates how far incomes need to rise or costs of new supply should fall before we get even close to the situation that prevailed for most of our history. It’s a big challenge.

Another great article . Appreciate your posts keep them coming the more people are informed the less likely they are to be caught in the bubble when it pops & pop it will.

ReplyDeleteWhere is the information sourced that states 2/3 of people in this country earn under $52,000 between 25 -32 years of age and are these people ready to buy as that demographics would have a huge number of students in it.?

ReplyDeleteGraham. Salary data is from ABS info. The 25-32 age demographic would have very few students in it. Most students start UNI or TAFE Studies @ 18 & very few do courses over 7 years, by 25 most are in work. In fact the majority of First Home Buyers are in the 25-32 age group. You also need to bear in mind most get married & start families in this age group & as a result have income reduced by leaving workforce or if still in the workforce paying 70% + of one income in childcare

DeleteWhy use Urban Economics as a source of income instead of the ABS.? Hard to see a workable solution beyond not everyone living in the large cities.

ReplyDeleteUrban Economics is using ABS Data when compiling their numbers. Urban Economics have has compiled the data for the Author & he is giving them credit for it.

DeleteMoving out of major cities is not the solution , no jobs, schools, health care, age care, infrastructure etc etc etc

Many of the smaller towns of Australia have infrastructure, schools , hospitals and aged care etc .

ReplyDeleteWith the people come the jobs and investment to smaller areas. A city that allowed to sprawl and then infilled is no solution.

Demograhica is not a source of information that holds its ground under scrutiny . It ignores wage to price ratio's in many countries that do not support its own argument.

Not so sure of that Bob. The reality is that you need to have sufficient income to service a debt. Let's say someone is on $100,000 per year. A 5x gross income house is $500,000. With a 10% deposit (and assuming stamp duty and other costs are met exactly by the FHBG) the debt is $450,000. For a 30 year mortgage, assuming a 5% interest rate (I'm being very generous) the monthly repayment is $2415.70. This is a weekly payment of $560. If the interest rate is 6%, this increases to $625 per week. Including HECS, the tax on that income is $34447, leaving $65553 or $1260.63 per week. This means the mortgage cost is about 50% of weekly net income at a rate of 6% or 44% at a rate of 5%. When I went to take out my mortgage, the bank told me their limit was 40% of net income in repayments. So by our normal bank rules, the 5x figure would seem to be the upper limit of affordability even with current low interest rates.

DeleteYour comment about smaller towns is a little misleading. You cannot move there and by a house without an income. You either take one of the jobs there, or start a business. You do not just move their, and expect that one day you'll get a job as others do what you've done. Historically people move to where the work is, or where they opportunities are, not move some place and assume the opportunities will find them. A better move would be the original idea for Joondalup, the satellite town concept. But seriously, if we do not want urban sprawl (the small towns will have it if you move people from the cities there) then we need to rethink the mass immigration policies. If you want more people, governments need to accept they will need a place to live.